Smart Routing in Payment Systems: How It Boosts Acceptance Rate

Every declined transaction is lost revenue. Industry data consistently shows that online merchants lose a meaningful share of potential transactions to technical processor declines, incorrect routing, or individual acquirer limits — losses entirely unrelated to customer intent or card validity. Smart routing is the architectural solution that addresses this systematically.

A declined transaction is not a customer saying no. It is your payment infrastructure saying it cannot handle the request — a fixable engineering problem.

What Smart Routing Actually Means

Smart routing — or intelligent transaction routing — is an algorithm that analyses an incoming transaction in real time and selects the optimal processing route from several available options. 'Optimal' is defined as the route most likely to approve the transaction, at the lowest fee, with the fastest settlement.

The algorithm evaluates: the card network and BIN of the payer, their country and transaction currency, the merchant category code (MCC), the historical approval rate of each route for this specific transaction profile, current processor load and availability status, and fraud risk signals.

TODA Pay implements this logic at the core of its payment orchestration architecture, routing every transaction through the highest-probability channel from a network of connected processors — automatically, in milliseconds.

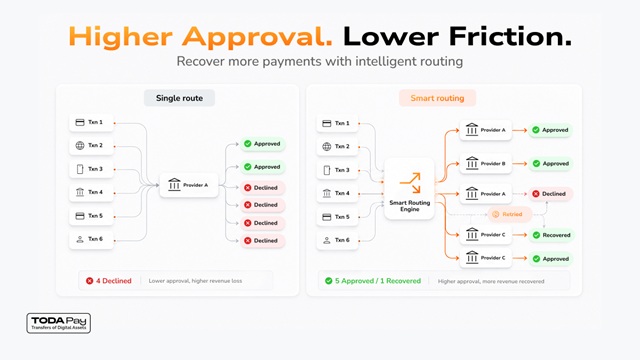

Why Relying on a Single Processor Is a Business Risk

Most smaller online businesses connect to a single PSP. If that PSP experiences a technical outage, a temporary BIN-range block, or a risk decision that affects your merchant account — every transaction during that window fails. There is no fallback.

Payment orchestration solves this architecturally. The merchant connects to a platform aggregating multiple processors. Smart routing selects between them in real time; cascade routing switches to the next in line if the first declines. The merchant processes continuously; the user experiences minimal friction.

Cascade Routing in Practice

Consider a practical example: a player from Germany attempts to deposit on an iGaming platform via a Mastercard issued by a regional German bank. The smart routing algorithm:

- Identifies the BIN as a German Mastercard, selects Route A — highest historical approval rate for DE-Mastercard transactions

- Route A declines (acquirer daily limit reached)

- System instantly cascades to Route B — an Open Banking connection to the player's bank via PSD2

- Transaction approved. The player sees a 2-second delay, not a decline message

The entire process is invisible to the end user. From the merchant's perspective, a sale that would have been permanently lost is recovered automatically.

The Financial Impact

The commercial case for smart routing is straightforward to model. As an illustrative example: a merchant processing $500,000 per month with a 10% technical decline rate would be losing $50,000 in potential revenue monthly. Payment orchestration with smart routing has the potential to recover a significant portion of technical declines — recovering $25,000–$35,000 is an illustrative range based on recovery rates observed in practice, though actual results will vary by merchant category, payment mix, and geographic distribution.

For high-risk merchants in iGaming and forex, where technical decline rates can run higher than the industry average, the potential impact is proportionally greater. TODA Pay's payment orchestration architecture is specifically designed for this environment.

FTD vs Trusted User Routing: Advanced Segmentation

Advanced payment providers apply smart routing not only at the processor level but at the user profile level. This distinction is critical for iGaming and subscription businesses.

A First Time Depositor (FTD) — a new user with no transaction history on the platform — carries an unknown fraud profile. Routing this traffic through a channel with more stringent verification reduces fraud exposure but may add marginal friction.

A Trusted User — a player with a history of successful deposits and no fraud flags — should be routed through the fastest, lowest-friction channel available. Applying the same friction to both user types is a conversion inefficiency.

TODA Pay implements this segmentation within its routing logic, separating FTD traffic from retention traffic. The goal: reduced fraud exposure for new users while minimising friction for loyal customers.

Level II / Level III Data and Interchange Optimisation

For B2B merchants processing corporate card transactions, smart routing intersects with interchange optimisation. By ensuring Level II data (tax ID, customer code) and Level III data (line-item details, tax amount) are passed correctly during authorisation, merchants may qualify for lower interchange rates on commercial card transactions.

TODA Pay's merchant payment services support Level II/III data passing for eligible transaction types, enabling B2B platforms and high-ticket merchants to potentially reduce processing costs beyond what basic routing improvements deliver.

What to Look for in a Smart Routing Provider

Not every PSP that uses the term 'smart routing' delivers the architecture behind it. When evaluating providers, verify:

- Processor pool depth — a minimum of 3–5 live processors for genuine diversification

- Real-time cascade rules — routing decisions made at transaction time, not pre-scheduled batches

- Custom routing logic — the ability to define rules by country, BIN range, amount, MCC, or user segment

- Decline reason analytics — visibility into why each transaction was declined and through which route

- FTD/retention segmentation — whether the system treats first-time and returning users differently

Providers offering a single processor with smart routing marketing copy are masking the problem, not solving it. TODA Pay's orchestration layer connects to a multi-processor network with full cascade logic, custom routing rules, and per-route analytics surfaced in a unified merchant dashboard.

Final Thoughts

For merchants processing above $100,000 per month, smart routing is baseline infrastructure rather than an optional add-on. The investment in a proper payment orchestration platform — or in switching to a PSP that provides it natively — can pay back quickly through recovered declined transactions, though specific timelines will depend on the merchant's current decline profile and processing mix.

Select a PSP partner that can share real acceptance rate data from merchants operating in your specific industry — not marketing slides, but measurable outcomes from comparable businesses. That is the standard TODA Pay holds itself to when engaging prospective partners.

About TODA Pay: TODA Pay (todapay.com) is a Payment Service Provider and payment orchestration platform built for high-volume and high-risk merchants. Operating under Canadian MSB and Polish EMI licences, TODA Pay delivers smart routing, Open Banking, APM, and crypto settlement through a single API integration.

DISCLOSURE: This content is produced in partnership with TODA Pay (todapay.com). All factual claims have been verified against publicly available data and company-provided information.